IIA IIA-CIA-Part2 Internal Audit Engagement Exam Practice Test

Internal Audit Engagement Questions and Answers

After finalizing an assurance engagement concerning safety operations in the oil mining process, the audit team concluded that no key controls were compromised. However, some opportunities for improvement were noted. Which of the following would be the most appropriate way for the chief audit executive (CAE) to report these results?

Which of the following is the primary reason the chief audit executive should consider the organization ' s strategic plans when developing the annual audit plan?

The chief audit executive (CAF) determined that the residual risk identified in an assurance engagement is acceptable. When should this be communicated to senior management?

Which of the following represents a ratio that measures short-term debt-paying ability?

According to IIA guidance, which of the following would not be a consideration for the internal audit activity (IAA) when determining the need to follow-up on recommendations?

Which of the following best demonstrates that the internal audit activity is using due professional care?

During follow-up, the chief audit executive (CAE) is having a discussion with management about the internal audit team ' s recommendations related to a significant issue Management accepted the issue but took no remedial action What is the next step for the CAE?

According to IIA guidance, which of the following activities is most likely to enhance stakeholders ' perception of the value the internal audit activity (IAA) adds to the organization?

1. The IAA uses computer-assisted audit techniques and IT applications.

2. The IAA uses a consistent risk-based approach in both its planning and engagement execution.

3. The IAA demonstrates the ability to build strong and constructive relationships with audit clients.

4. The IAA frequently is involved in various project teams and task forces in an advisory capacity.

Which of the following is the primary reason for internal auditors to conduct interim communications with management of the area under review?

An internal auditor s examination of accounts receivable generates the following results:

What is the projected misstatement for the population if ratio estimation is used?

Which of the following factors should a chief audit executive consider when determining the audit universe?

1. Components of the organization ' s strategic plan.

2. Inputs from senior management and the board.

3. Views of competitors and business associates.

4. Results of exit interviews with departing employees.

Which of the following activities would an internal auditor perform as a consulting engagement for an organization?

Which of the following is an example of a properly supervised engagement?

An organization ' s board would like to establish a formal risk management function and has asked the chief audit executive (CAE) to be involved in the process. According to IIA guidance, which of the following roles should the CAE not undertake?

According to IIA guidance, which of re following actions should the internal auditor take immediately after having considered fraud scenarios and identified and prioritized fraud risks?

An internal auditor is starting the fieldwork of an assurance engagement. The auditor will conduct a walkthrough of selected controls with control owners. What should be the primary objective of this walkthrough?

An internal audit activity maintains a quality assurance and improvement program that includes annual self-assessments The internal audit activity includes in each engagement report a clause that the engagement is conducted in conformance with the International Standards for the Professional Practice of Internal Auditing (Standards). Which of the following justifies inclusion of this clause in the reports?

According to IIA guidance, which of the following statements is true regarding reporting the results of the quality assurance and improvement program?

Which of the following is not a primary purpose for conducting a walk-through during the initial stages of an assurance engagement?

Which of the following would most likely cause an internal auditor to consider adding fraud work steps to the audit program?

An internal audit activity has to confirm the validity of the activities reported by a grantee that received a charitable contribution from the organization. Which of the following methods would best help meet this objective?

Which of the following statements best explains why an internal auditor should pay attention to retained earnings of an organization?

According to IIA guidance, which of the following is true regarding typical fraud schemes?

1.A diversion occurs when an employee has an undisclosed personal economic interest in a transaction that adversely affects the organization

2.Tax evasion is intentional reporting of false or misleading information on a tax return by an organization to reduce taxes owed.

3.Skimming involves stealing cash or assets from the organization and is normally concealed by adjusting the organization’s records

4Disbursement fraud occurs when a person causes the organization to issue a payment for fictitious goods or services

According to IIA guidance, which of the following statements is true regarding engagement planning?

An internal auditor is planning to audit the organization ' s payroll function, which was recently outsourced. Which of the following is the most appropriate first step for the auditor?

An employee in the sales department completes a purchase requisition and forwards it to the purchaser. The purchaser places competitive bids and orders the requested items using approved purchase orders. When the employee receives the ordered items, she forwards the packing slips to the accounts payable department. The invoice for the ordered items is sent directly to the sales department, and an administrative assistant in the sales department forwards the invoices to the accounts payable department for payment. Which of the following audit steps best addresses the risk of fraud in the cash receipts process?

Which of the following is the most important determinant of the objectives and scope of assurance engagements?

The organizational chart, business objectives, and policies and procedures of the area to be reviewed

Senior management requested that the internal audit activity perform a consulting project to assist in making a decision on a new software system. Which of the following would be used to determine the engagement objectives?

Acceding to IIA guidance, when of the Mowing is an assurance service commonly performed by the internal audit activity?

While reviewing the workpapers and draft report from an audit engagement, the chief audit executive (CAE) found that an Important compensating control had not been considered adequately by the audit team when it reported a major control weakness Therefore, the CAE returned the documentation to the auditor in charge for correction Based on this Information, which of the following sections of the workpapers most likely would require changes?

1.Effect of the control weakness.

2.Cause of the control weakness

3.Conclusion on the control weakness.

4.Recommendation for the control weakness.

Which of the following manual audit approaches describes testing the validity of a document by following it backward to a previously prepared record?

According to IIA guidance, which of the following is true regarding audit supervision?

1. Supervision should be performed throughout the planning, examination, evaluation, communication, and follow-up stages of the audit engagement.

2. Supervision should extend to training, time reporting, and expense control, as well as administrative matters.

3. Supervision should include review of engagement workpapers, with documented evidence of the review.

An internal auditor examined a nostatistical sample of open accounts receivable balances and discovered that 10 out of 60 exceeded the approved unseated credit limit threshold defined by the organization ' s policy What should the auditor document in the workpapers?

The internal audit activity plans to assess the effectiveness of management’s self-assessment activities regarding the risk management process. Which of the following procedures would be most appropriate to accomplish this objective?

According to IIA guidance, which of the following best describes the purpose of a planning memorandum for an audit engagement?

According to the IIA guidance, which of the following foes the engagement work test in a review in a review of an organization al process?

According to IIA guidance, which of the following strategies would add the least value to the achievement of the internal audit activity ' s (IAA ' s) objectives?

According to IIA guidance,which of the following is true about the supervising internal auditor ' s review notes?

• They are discussed with management prior to finalizing the audit.

• They may be discarded after working papers are amended as appropriate.

• They are created by the auditor to support her fieldwork in case of questions.

• They are not required to support observations issued in the audit report.

In a small internal audit function, a single auditor is responsible for conducting the entire audit engagement. In this situation, what is the benefit of using a checklist as part of an engagement work program?

Which of the following reasonably represents best practices regarding what should be the level of internal audit resource investment in monitoring and following up on engagement outcomes?

During a review of the organization ' s waste management processes, the internal auditor discovered that wastewater is being disposed of inappropriately. The auditor ' s recommendations, suggested to mitigate the risk of regulatory sanctions and reputational damages, were accepted and timelines for implementation were agreed. However, during the internal audit activity ' s periodic follow-up exercise, management indicated that the recommendation was too expensive to implement and the current disposal method has been cost-effective. What should the chief audit executive do in this case?

Which of the following recommendation types is most likely to propose the most long-term solutions?

The following is a list of major findings in the executive summary report for an audit of the contract management process

- Noncompliance with contract provisions requiring vendors to obtain insurance policies with indemnity value of not less than $1 million

- Compliance with contract obligations and deliverables is not monitored

- No contract agreement with five vendors providing core services

Which of the following is an appropriate conclusion that can be drawn from these findings?

Which of the following represents the best example of a strategic goal?

An internal auditor of a construction organization found that completed inspection results, required by the organization ' s policy, were missing from the computer system. Which of the following, if included in the audit report, would demonstrate that the auditor performed a root cause analysis of this observation?

An organization s inventory is stored m multiple warehouses. During an inventory audit which of the following activities would most benefit from the use of computerized audit tools?

A newly appointed chief audit executive (CAE) started analyzing the organization ' s policies in an attempt to customize them to address internal audit specifics. Which of the following organizationwide practices is most likely to be acceptable to the CAE?

Which of the following is least likely to help ensure that risk is considered in a work program?

An internal auditor and engagement client are deadlocked over the auditor ' s differing opinion with management on the adequacy of access controls for a major system. Which of the following strategies would be the most helpful in resolving this dispute?

Which of the following computerized audit tools or techniques should be used if the internal auditor wants to extract specific files and records in the database?

An internal audit activity has to confirm the validity of the activities reported by a grantee that received a chantable contribution from the organization Which of the following methods would best help meet this objective?

Which of the following statements is true regarding the use of internal control questionnaires (ICOs)?

New environmental regulations require the board to certify that the organization ' s reported pollutant emissions data is accurate. The chief audit executive (CAE) is planning an audit to provide assurance over the organization ' s compliance with the environmental regulations. Which of the following groups or individuals is most important for the CAE to consult to determine the scope of the audit?

According to IIA guidance, which of the following statements about analytical procedures is true?

The human resources (HR) department was last reviewed three years ago and is due for an assurance engagement after undergoing recent process changes. Which of the following would the most effective option identify the HR department ' s risks and controls?

Which of the following is an example of a properly supervised engagement?

A manufacturing organization specializes in the production of evaporated milk and breakfast cereals. The manufacturing processes create significant loss in the form of waste and byproducts. The provision for normal production loss is known to senior management, but little action is taken when abnormal production losses occur. The organization sells its production byproducts to fish farmers at a reduced price. The byproducts are a widely recognized and used product in the fish farming industry. The organization has a policy that also allows its employees to purchase the byproducts at a negligible price. Based on the above, which of the following risks should the internal audit function consider when planning an engagement of the production process?

When reviewing workpapers, engagement supervisors may ask for additional evidence or clarification via review notes. According to IIA guidance, which of the following statements is true regarding the engagement supervisor’s review notes?

During the filework phase of an assurance engagement the internal auditor decides that she wants to adjust the audit work program. Which of the following is the most appropriate next step for the auditor to take9

Management testimony of improper segregation of duties in the cash receipt process can be considered which of the following?

According to the International Professional Practices Framework, which of the following is an appropriate reason for issuing an interim report?

To keep management informed of audit progress when audit engagements extend over a long period of time.

To provide an alternative to a final report for limited-scope audit engagements.

To communicate a change in engagement scope for the activity under review.

The audit plan of an internal audit function includes an assurance engagement of the organization’s cybersecurity protocols. However, the engagement supervisor assigned to execute the engagement identifies that the internal auditors with competencies in cybersecurity are scheduled for upcoming leave and are involved in other engagements. Those auditors would not be available to participate in the cybersecurity engagement. Which of the following would be the appropriate action for the engagement supervisor?

Which of the following is a true statement regarding the use of flowcharts as an audit tool?

Which of the following best describes the manual audit procedure known as vouching?

After completing an assurance engagement, the chief audit executive (CAE) concludes that management has accepted a level of risk that may be unacceptable to the

organization. What is the most appropriate first step for the CAE to take?

Which of the following is an example of internal benchmarking?

A chief audit executive is preparing interview questions for the upcoming recruitment of a senior internal auditor. According to IIA guidance, which of the following attributes shows a candidate ' s ability to probe further when reviewing incidents that have the appearance of misbehavior?

Which of the following conditions are necessary for successful change management?

1. Decisions and necessary actions are taken promptly.

2. The traditions of the organization are respected.

3. Changes result in improvement or reform.

4. Internal and external communications are controlled.

A corporate merger decision prompts the cruel audit executive (CAE) to propose interim changes lo the existing annual audit plan to account for emerging risks. When of the following is the most appropriate action for the CAE to take regarding the changes made to the audit plan?

An internal auditor at a bank informed the branch manager of a malfunctioning lock on one of the vaults. The risk associated with this issue was deemed significant by the chief audit executive (CAE), and immediate remediation was recommended However during a follow-up engagement the branch manager told the CAE that the risk was actually not significant, hence no action was taken. What is the most appropriate next step for the CAE?

An engagement team is being assembled to audit of one of the organization ' s vendors Which of the following statements best applies to this scenario?

Which of the following offers the best explanation of why the auditor in charge would assign a junior auditor to complete a complex part of the audit engagement?

Senior IT management requests the internal audit activity to perform an audit of a complex IT area. The chief audit executive (CAE) knows that the internal audit activity lacks the expertise to perform the engagement. Which of the following is the most appropriate action for the CAE to take?

Which of the following statements is false regarding roles and responsibilities pertaining to risk management and control?

When reviewing workpapers, engagement supervisors may ask for additional evidence or clarification via review notes. According to IIA guidance, which of the following statements is true regarding the engagement supervisors review notes?

Which of the following should be described in the recognition element of a typical internal audit repot?

A newly appointed chief audit executive (CAE) of a small organization is developing a resource management plan Which of the following approaches would be most beneficial to help the CAE obtain details of the Internal audit activity ' s collective knowledge skills, and other competencies?

Which of the following statements is true regarding an organization’s inventory valuation?

Which of the following audit steps would an internal auditor perform when reviewing cash disbursements to satisfy IIA guidance on due professional care?

According to IIA guidance, when would an interim report typically be produced?

In which of the following situations would an internal auditor consider the need to outsource competencies and skills9

If there is a significant error or omission in the final audit report that was communicated to management, which of the following is the key action for the internal audit activity?

Which of the following internal audit activities is performed in the design evaluation phase?

An internal audit engagement supervisor approved the engagement work program submitted by an internal auditor and concluded that it satisfied engagement objectives. At the end of the engagement, the engagement supervisor reviewed the completed work program and found numerous deficiencies and inconsistencies in the engagement workpapers. Which of the following should be improved in the process of engagement supervision?

In which of the following ways can the internal audit activity new engagement opportunities?

A chief audit executive (CAE) received a detailed internal report of senior management ' s internal control assessment. Which of the following subsequent actions by the CAE would provide the greatest assurance over management ' s assertions?

Which of the following statements best describes the difference between risk appetite and risk tolerance?

The internal audit manager has been delegated the task of preparing the annual internal audit plan for the forthcoming fiscal year. All engagements should be appropriately categorized and presented to the chief audit executive for review. Which of the following would most likely be classified as a consulting engagement?

The engagement supervisor would like lo change the audit program ' s scope poor to beginning fieldwork According to IIA guidance before any change is implemented what is the most important action that should be undertaken?

An engagement work program o of greatest value to audit management when which of the following is true?

When taken by a chief audit executive, which of the following actions would be most likely to prevent division management from exaggerating sales reports

1.Announcing a series of internal audit engagements focusing on compliance with corporate sales-reporting policies.

2.Asking the president and the board to issue a statement of corporate policy stressing the importance of accurate management reporting and the negative consequences of intentional misreporting

3.Setting up a hotline for employees to report fraudulent behavior anonymously.

4.Assisting the controller in developing and monitoring a series of business process indicators, which are historically correlated with, but independent of. sales.

The board of directors of a global organization has found an increased number of reported cases of unethical practices since last year. To assist the board in gaining a better understanding of the degree of ethics awareness within the organization, which of the following actions should be undertaken?

An internal auditor completed a consulting engagement covering a recent advertising campaign. The audit client asked the auditor to forward a copy of the report to one of the three advertising agencies used by the organization. According to IIA guidance, which of the following statements is true regarding this request?

An internal auditor is conducting an initial risk assessment of an audit area and wants to assess management ' s compliance with privacy laws for safeguarding customer information stored on the organization ' s servers. Which course of action is appropriate for this phase of the engagement?

An internal auditor wanted to determine whether company vehicles were being used for personal purposes She extracted a report that listed company vehicle numbers business units to which the vehicles are allocated travel dates, travel duration and mileage She then filtered the data for weekend dates Which of the following additional information would the auditor need?

Which of the following approaches would best help an internal auditor determine whether a retailer database of 100,000 customers has nay duplicate accounts?

White planning an audit engagement of a procurement card activity. which of the following actions should an internal auditor take to denary relevant risks and controls?

The chief audit executive (CAE) determined that the internal audit activity lacks the resources needed to complete the internal audit plan Which of the following would be the most appropriate action tor the CAE to take?

During a consulting engagement an internal auditor wants to determine whether all principal stakeholders are involved in a project. Which tool should the auditor use?

Due to a recent system upgrade, an audit is planned to test the payroll process. Which of the following audit objectives would be most important to prevent fraud?

Which of the following data analysis techniques is used to identify inappropriately matching values, such as names, addresses, and account numbers in disparate systems?

When auditing an organization ' s purchasing function, which of the following appropriately matches an engagement objective and the resulting audit procedure?

During an assurance engagement, an internal auditor noted that the time staff spent accessing customer information in large Excel spreadsheets could be reduced significantly through the use of macros. The auditor would like to train staff on how to use the macros. Which of the following is the most appropriate course of action for the internal auditor to take?

Which of the following contributes to the reliability of information collected for an audit engagement?

Which of the following sources of testimonial evidence would be considered the most reliable regarding whether a process is effectively performed according to its design?

While conducting a review of the logistics department the internal audit team identified a crucial control weakness. The chief audit executive (CAE) decided to prepare an audit memorandum for management of the logistics department followed by an informal meeting What is the most likely reason the CAE decided to prepare the audit memorandum?

In the years after the mid-service point of a depreciable asset, which of the following depreciation methods will result in the highest depreciation expense?

Which of the following would most likely form part of the engagement scope?

Which phase of an audit engagement is typically the most effective time for an internal auditor to develop a risk and control matrix?

An organization has a mature control environment but limited internal audit resources. Given this scenario, on which of the following should the internal auditors focus their testing?

Operational management In the IT department has developed key performance indicator reports, which are reviewed in detail during monthly staff meetings. This activity is designed to prevent which of the following conditions?

What is a control implication for an organization that adopts a flat structure?

According to IIA guidance, which of the following statements is false regarding a review of the controls in place to prevent fraud?

Which of the following has the greatest effect on the efficiency of an audit?

Which of the following would not be a typical activity for the chief audit executive to perform following an audit engagement?

According to IIA guidance, which of the following is based on the results of a preliminary assessment of risks relevant to the area under review?

An organization ' s chief audit executive is developing an integrated audit approach to provide value-added services that can help the organization meet its strategic objectives and goals. Which of the following is an advantage of using an integrated audit approach that assists the organization?

When determining the level of staff and resources to be dedicated to an assurance engagement, which of the following would be the most relevant to the chief audit executive?

The board has asked the internal audit activity (IAA) to be involved in the organization ' s enterprise risk management process. Which of the following activities is appropriate for IAA to perform without safeguards?

An organization has a mature control environment but limited internal audit resources Given this scenario, on which of the following should the internal auditors focus their testing?

An internal auditor plans to conduct a walk-through to evaluate the control design of a process. Which of the following techniques is the auditor most likely to use?

Which of the following best demonstrates internal auditors performing their work with proficiency?

In preparing the engagement work program, which of the following is generally true with respect to secondary controls?

What is the primary purpose of creating a preliminary draft audit report?

Which of the following is the most appropriate approach for the internal audit activity to follow up on management action plans?

If observed during fieldwork by an internal auditor, which of the following activities is least important to communicate formally to the chief audit executive?

An internal auditor wants to assess whether the organization ' s governing body was involved in strategic decisions for the use of social media. What could provide the most relevant evidence?

A toy manufacturer receives certain components from an overseas supplier and uses them to assemble final products Recently quality reviews have identified numerous issues regarding the components ' compliance with mandatory quality standards. Which type of engagement would be most appropriate to assess the root causes of the quality issues?

A bank uses customer departmentalization to categorize its departments. Which of the following groups best exemplifies this method of categorization?

Which of the following is essential for ensuring that the internal audit activity ' s findings and recommendations receive adequate consideration?

Which of the following parties is accountable for ensuring adequate support for conclusions and opinions readied by the internal audit activity while relying on external auditors ' work?

Which of the following risk assessment approaches involves gathering data from work team representing different levels of an organisation?

A newly promoted chief audit executive (CAE) is faced with a backlog of assurance engagement reports to review for approval. In an attempt to attach a priority for this review, the CAE scans the opinion statement on each report. According to IIA guidance, which of the following opinions would receive the lowest review priority?

1. Graded positive opinion.

2. Negative assurance opinion.

3. Limited assurance opinion.

4. Third-party opinion.

' Internal policy prohibits employees from entering into contacts with financial obligations without proper approval.

A project manager signed a change to an important service agreement without obtaining the proper approval As a result the organization is receiving $5,000 per month less for its services.’’

Which of the following should be added to the observation?

Which of the following statements is true regarding internal auditors and other assurance providers?

Which of the following methods is most closely associated to year over year trends?

Organizations that adopt just-in-time purchasing systems often experience which of the following?

According to IIA guidance, which of the following statements about analytical procedures is true?

Which of the following sampling techniques is typically used when an internal auditor wants to test a large sample for fraud?

A chief audit executive (CAE) reviews the supervision of an internal audit engagement Which of the following would most likely assure the CAE that the engagement had adequate supervision?

During a fraud interview, it was discovered that unquestioned authority enabled a vice president to steal funds from the organization. Which of the following best describes this condition?

Which of the following is true of matrix organizations?

Which of the following internal control attributes should internal auditors consider testing during a review of the board of directors?

In which of the following populations would the internal auditor most likely choose to use a stratified sampling approach?

Considering the five-attribute approach to documenting deficiencies in an area under review which of the following answers the question. " What should be in place?’’

An internal auditor is performing an engagement to determine whether quality control checks of electronic gaming systems are performed consistently among a technology company’s factories. Which of the following tests would support the audit engagement objectives?

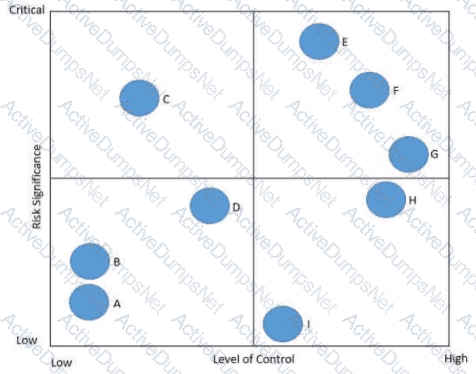

In the following risk control map risks have been categorized based on the level of significance and the associated level of control. Which of the following statements is true regarding Risk C?

When auditing an organization ' s cash-handling activates which of the following is the most reliable form of testimonial evidence an internal auditor can obtain?

According to the IIA Code of Ethics, which of the following is required with regard to communicating results?

A manufacturer is under contract to produce and deliver a number of aircraft to a major airline. As part of the contract, the manufacturer is also providing training to the airline ' s pilots. At the time of the audit, the delivery of the aircraft had fallen substantially behind schedule while the training had already been completed. If half of the aircraft under contract have been delivered, which of the following should the internal auditor expect to be accounted for in the general ledger?

A corporate merger decision prompts the chief audit executive (CAE) to propose interm changes to the existing annual audit plan to account for emerging risks Which of the following Is the most appropriate action for the CAE to take regarding the changes made to the audit plan?

During the review of an organization ' s retail fraud deterrence program, an employee mentions that an expensive fraud surveillance information system is rarely used. The internal auditor concludes that additional staff are required to properly utilize the system to its full potential. According to IIA guidance, which criteria for evidence is most lacking to reach this conclusion?

Senior management decides to adopt a conservative working capital policy. What would be the expected result for the organization?

While conducting an engagement in the procurement department, the internal auditor noticed that the department head’s travel reports showed minor travel expenses, and there were no charges for hotels, meals, or transportation However, the auditor knew that the department head frequently traveled worldwide to meet with suppliers and visit their production sites. Which of the following would be the most appropriate next step for the auditor?

A chief audit executive (CAE) a developing a work program for an upcoming engagement that will review an organization’s small contracting services. When of the following would the CAT need to consider most when developing the work program?

According to IIA guidance, which of the following is a limitation of a heat map?

Which of the following should be included in a company ' s year-end inventory valuation?

An internal auditor is conducting a review of the procurement function and uncovers a potential conflict of interest between the chief operating officer and a significant supplier of IT software development services. Which of the following actions is most appropriate for the internal auditor to take?

Which of the following statistical sampling approaches is the most appropriate for testing a population for fraud?

The final engagement communication contains the following observation:

The internal auditor discovered that three of the 10 contracts reviewed failed to meet the organization ' s competitive bidding requirements Management explained that senior management deemed these purchases to be critical and awarded them as sole-source. "

Which of the following components is missing in the documentation of the observation?

Which of the following statements is true regarding engagement planning?

Which of the following is true regarding the communication of engagement results with stakeholders?

During the preliminary survey of the procurement department, an internal auditor noted a major control weakness in the organization ' s ordering and receiving process. According to IIA guidance, which of the following is the most appropriate action the internal auditor should take?

The internal audit function is performing an assurance engagement on the organization’s environmental, social, and governance (ESG) program. The engagement objective is to determine whether the ESG program’s activities are meeting the program’s established goals. The internal audit function has completed a risk and control assessment of the ESG program ' s activities. What is the appropriate next step?

During an internal audit engagement, which of the following is true regarding the decision to use statistical sampling or nonstatistical sampling?

A chief audit executive (CAE) identifies that the internal audit activity lacks a necessary skill to perform a management request for a consulting engagement. According to IIA guidance, which of the following Is the most appropriate action the CAE should take regarding the request?

Which of the following factors would the auditor in charge be least likely to consider when assigning tasks to audit team members for an engagement?

The chief audit executive (CAE) should determine whether the internal audit activity has confirmed the status of all of management ' s corrective actions Doing so would help the CAE assess which of the following?

A chief audit executive ' s report to the board showed a significant trend of recent aud4s going over planned budgeted hours. Which of the following factors could cause this trend?

Which of the following scenarios is an example of appropriate engagement supervision?

An internal auditor suspects that a program contains unauthorized code or errors. Which of the following would assist the internal auditor in this regard?

Which of the following technologies will best reduce human processing errors and enable seamless exchange of business transactions among business partners?

According to the Standards, which of the following is true regarding the auditor ' s inclusion of management ' s satisfactory performance in the final audit report?

According to IIA guidance, which of the following procedures would be least effective in managing the risk of payroll fraud?

A large retail organization, which sells most of its products online, experiences a computer hacking incident. The chief IT officer immediately investigates the incident and concludes that the attempt was not successful. The chief audit executive (CAE) learns of the attack in a casual conversation with an IT auditor. Which of the following actions should the CAE take?

1. Meet with the chief IT officer to discuss the report and control improvements that will be implemented as a result of the security breach, if any.

2. Immediately inform the chair of the audit committee of the security breach, because thus far only the chief IT officer is aware of the incident.

3. Meet with the IT auditor to develop an appropriate audit program to review the organization ' s Internet-based sales process and key controls.

4. Include the incident in the next quarterly report to the audit committee.

Which of the following activities Is most likely to require a fraud specialist to supplement the knowledge and skills of the internal audit activity?

Which of the following is not a direct benefit of control self-assessment (CSA)?

Which of the following is the next step in understanding a business process once an internal auditor has identified the process?

Which of the following is the most important concept to be included in a consulting engagement agreement?

According to IIA guidance, which of the following accurately describes the responsibilities of the chief audit executive with respect to the final audit report?

1. Coordinate post-engagement conferences to discuss the final audit report with management.

2. Include management ' s responses in the final audit report.

3. Review and approve the final audit report.

4. Determine who will receive the final audit report.

Which of the following best describes how an internal auditor would use a flowchart during engagement planning?

Following an IT systems audit, management agreed to implement a specific control in one of the IT systems. After a period, the internal auditor followed up and learned that management had not implemented the agreed management action due to the decision to move to another IT system that has built-in controls, which may address the risks highlighted by the internal audit. Which of the following is the most appropriate action to address the outstanding audit recommendation?

Following an IT systems audit, management agreed to implement a specific control in one of the IT systems. After a period, the internal auditor followed up and learned that management had not implemented the agreed management action due to the decision to move to another IT system that has built-in controls, which may address this risks highlighted by the Internal audit Which of the following Is the most appropriate action to address the outstanding audit recommendation?

An engagement supervisor obtains facilities maintenance reports from a contractor during an audit of third-party services. Which of the following is the source of authority for the engagement supervisor to make such contact outside the organization?

In which of the following situations would an internal control questionnaire best suit the internal auditor ' s purpose?

Management would like to self-assess the overall effectiveness of the controls in place for its 200-person manufacturing department Which of the following client-facilitated approaches is likely to be the most efficient way to accomplish this objective?

Which of the followings statements describes a best practice regarding assurance engagement communication activities?

Which of the following describes (he primary reason why a preliminary risk assessment is conducted during engagement planning?

Which of the following best describes why an internal audit activity would consider sending written preliminary observations to the audit client?

According to IIA guidance, which of the following describes the primary reason the chief audit executive (CAE) should actively network and build relationships with senior management and the board?

Which of the following documents are internal auditors most likely to be asked to sign as a demonstration of due professional care?

Which of the following is one of the five attributes that internal auditors include when documenting a deficiency?

During a previous audit engagement, an internal auditor recommended that management implement a whistleblowing process. During follow-up, the auditor discovered that the process has been outsourced. Which of the following is the most appropriate response for the internal auditor?

According to IIA guidance, when of the Mowing statements is true regarding an engagement supervisor ' s use of review notes?

Which of the following audit steps would an internal auditor most likely be questioned on?

An electric utility provider measures working time spent on processing grid connection applications, response time for electricity outages, and the call center queuing time. Which of the following criteria would better suit a customer-oriented provider for measurement?

What information would be most useful to an internal auditor who is attempting to identify specific processes to include in the scope of an assurance engagement?

An internal auditor is testing the success of the IT support department in meeting the service levels guaranteed to small, medium and large customers. The customer ' s size classification is based on its annual expenditures with the organization and the nature and extent of services it receives. Which of the following sampling techniques would be the most suitable to select customers for this test?

Which of the following is the advantage of using internal control questionnaires (ICQs) as part of a preliminary survey for an engagement?

The internal audit activity has adopted the balanced scorecard approach to assess its performance According to MA guidance which of the following is a key performance indicator relevant to the audit client?

Which of the following represents the best method for confirming that vendor invoices were for authorized purchases?

Which of the following behaviors could represent a significant ethical risk if exhibited by an organization ' s board?

1. Intervening during an audit involving ethical wrongdoing.

2. Discussing periodic reports of ethical breaches.

3. Authorizing an investigation of an unsafe product.

4. Negotiating a settlement of an employee claim for personal damages.

The chief audit executive was asked to define me internal audit activity s key performance indicators (KPIs) tor the upcoming year. The KPIs must measure efficiency and effectiveness. Which of the following is an example of a KPI that measures effectiveness?

An internal audit manager assigns an audit team to test purchase transactions by selecting a sample from transactions processed by each of the three procurement officers.

Which of the following techniques will help the audit team achieve this sampling objective?

According to IIA guidance, which of the following statements is true regarding engagement planning?

Which of the following best describes external benchmarking using trend analysis for a subsidiary of an international company?

An internal auditor has discovered that duplicate payments were made to one vendor Management has recouped the duplicate payments as a corrective action Which of the following describes managements action in this case?

An internal auditor receives a document displaying all the steps of a process and the path taken as transactions flow between each step of the process How is the internal auditor most likely to use This document during the engagement?

During an audit of the accounts receivable (AR) process, an internal auditor noted that reconciliations are still not performed regularly by the AR staff, a recommendation that was made following a previous audit. Monitoring by the financial reporting function has failed to detect the shortcoming. Both the financial reporting function and AR report to the controller, who is responsible for implementing action plans. Which of the following supports the internal auditor ' s decision to combine both observations into one reported finding?

The chief audit executive (CAE) for a manufacturing company included in this year s audit plan a review of the company ' s laboratory, using an experienced external service provider. The audit plan was approved by the audit committee without any changes At the time of engaging the external service provider, the CAE also secured the approval from the CEO. Who is responsible for ensuring that the conclusions reached for this exercise are adequately supported7

Which of the following processes does the board manage to ensure adequate governance?

An internal audit intends to create a risk and control matrix to better understand the organization ' s complex manufacturing process. With which of the following approaches would the auditor most likely start?

An internal auditor believes that the internal audit activity ' s independence is impaired Which of the following actions should the internal auditor take first?

What is the purpose of an internal control questionnaire?

Which of the following measures immediate short-term liquidity?

The chief audit executive can illustrate the value of the internal audit activity by reporting which of the following to the board?

An internal auditor discovered a control weakness that needs to be communicated to management. Which of the following is the best method for first communicating the weakness?

An audit reveals that a manager ' s spouse is receiving paychecks, but is not employed by the organization. According to IIA guidance, which of the following actions should the internal auditor take?

During the planning process for a human resources audit, an internal auditor obtains an organizational chart. The auditor observes a flat organizational structure. Which of the below risks should the auditor consider for this engagement?

According to IIA guidance, which of the following practices by the chief audit executive (CAE) best enhances the organizational independence of the Internal audit activity^

The board of directors expressed concerns about potential external risks that could impact the organization s ability to meet its annual objectives and goals The board requested consulting services from the internal audit activity to gain insight regarding the external risks Which of the following engagement objectives would be appropriate to fulfill this request?

An internal auditor is tasked with evaluating the adequacy of the organization ' s inventory fraud controls. What is the most relevant information that the auditor can obtain from the documentation of cyclic counting for this purpose?

During a review of data privacy an internal auditor is tasked with testing management ' s identification and prioritization of critical data collected by the organization. Which of the following steps would accomplish this objective?

An internal auditor is performing a review of an organization ' s vendor for any possible conflicts of interest. Which of the following would provide the greatest assistance to the auditor in meeting this objective?