IIA IIA-ACCA ACCA CIA Challenge Exam Exam Practice Test

ACCA CIA Challenge Exam Questions and Answers

Which of the following is a characteristic of just-in-time inventory management systems?

Which of the following most accurately describes the purpose of application authentication controls?

An internal auditor is reviewing physical and environmental controls for an IT organization. Which control activity should not be part of this review?

When auditing an application change control process, which of the following procedures should be included in the scope of the audit?

1. Ensure system change requests are formally initiated, documented, and approved.

2. Ensure processes are in place to prevent emergency changes from taking place.

3. Ensure changes are adequately tested before being placed into the production environment.

4. Evaluate whether the procedures for program change management are adequate.

Which of the following are typical audit considerations for a review of authentication?

1. Authentication policies and evaluation of controls transactions.

2. Management of passwords, independent reconciliation, and audit trail.

3. Control self-assessment tools used by management.

4. Independent verification of data integrity and accuracy.

Which of the following statements regarding program change management is not correct?

According to Porter, which of the following is associated with fragmented industries?

While reviewing the contracts for a large city, the internal auditor learns that the organization contracted to perform trash collection is paid based on the number of bins emptied each week As a result, the city has minimal control over payments Which of the following actions should the auditor recommend to give the city greater control over payments?

Which of the following statements about COBIT is not true?

Which of the following purchasing scenarios would gain the greatest benefit from implementing electronic data interchange?

According to IIA guidance on IT. which of the following plans would pair the identification of critical business processes with recovery time objectives?

The greatest advantage of functional departmentalization is that it:

Which of the following is not a barrier to effective communication?

The audit committee of a global corporation has mandated a change in the organization's business ethics policy. Which of the following approaches describes the best way to accomplish the policy's diffusion worldwide?

During an audit of the organization's annual financial statements, the internal auditor notes that the current cost of goods sold percentage is substantially higher than in prior years. Which of the following is the most likely explanation for this increase?

Which of the following are the most common characteristics of big data?

Operational management in the IT department has introduced performance evaluation policies that are linked to employees achieving continuing education hours. This activity is designed to prevent which of the following conditions?

When attempting to devise creative solutions to problems, team members initially should do which of the following?

Which of the following is a major advantage of decentralized organizations, compared to centralized organizations?

Which of the following best describes the purpose of disaster recovery planning?

Which of the following application software features is the least effective control to protect passwords?

An organization had three large centralized divisions: one that received customer orders for service work; one that scheduled the service work at customer locations; and one that answered customer calls about service problems. These three divisions were restructured into seven regional groups, each of which performed all three functions. One advantage of this restructuring would be:

According to MA guidance, which of the following would indicate poor change management control?

1. Low change success rate

2. Occasional planned outages

3. Low number of emergency changes.

4. Instances of unauthorized changes

Which of the following would be a risk in the development of end-user computing (EUC) applications, compared to traditional information systems?

Which of the following statements about matrix organizations is false?

Which of the following statements accurately describes the responsibility of the internal audit activity (IAA) regarding IT governance?

1. The IAA does not have any responsibility because IT governance is the responsibility of the board and senior management of the organization.

2. The IAA must assess whether the IT governance of the organization supports the organization’s strategies and objectives.

3. The IAA may assess whether the IT governance of the organization supports the organization’s strategies and objectives.

4. The IAA may accept requests from management to perform advisory services regarding how the IT governance of the organization supports the organization’s strategies and objectives.

The percentage of sales method, rather than the percentage of receivables method, would be used to estimate uncollectible accounts if an organization seeks to:

Which of the following are typical responsibilities for operational management within a risk management program?

1. Implementing corrective actions to address process deficiencies.

2. Identifying shifts in the organization's risk management environment.

3. Providing guidance and training on risk management processes.

4. Assessing the impact of mitigation strategies and activities.

Which of the following factors is considered a disadvantage of vertical integration?

A retail organization mistakenly did not include S10.000 of inventory in the physical count at the end of the year. What was the impact to the organization's financial statements?

An organization's internal audit plan includes a recurring assurance review of the human resources (HR) department. Which of the following statements is true regarding preliminary communication between the auditor in charge (AIC) and the HR department?

1. The AIC should notify HR management when the draft audit plan is being developed, as a courtesy.

2. The AIC should notify HR management before the planning stage begins.

3. The AIC should schedule formal status meetings with HR management at the start of the engagement.

4. The AIC should finalize the scope of the engagement before communicating with HR management.

When setting the scope for the identification and assessment of key risks and controls in a process, which of the following would be the least appropriate approach?

Which of the following recommendations made by the internal audit activity (IAA) is most likely to help prevent fraud?

A code of business conduct should include which of the following to increase its deterrent effect?

1. Appropriate descriptions of penalties for misconduct.

2. A notification that code of conduct violations may lead to criminal prosecution.

3. A description of violations that injure the interests of the employer.

4. A list of employees covered by the code of conduct.

According to IIA guidance, which of the following are the most important objectives for helping to ensure the appropriate completion of an engagement?

1. Coordinate audit team members to ensure the efficient execution of all engagement procedures.

2. Confirm engagement workpapers properly support the observations, recommendations, and conclusions.

3. Provide structured learning opportunities for engagement auditors when possible.

4. Ensure engagement objectives are reviewed for satisfactory achievement and are documented properly.

For which of the following fraud engagement activities would it be most appropriate to involve a forensic auditor?

The chief audit executive of a medium-sized financial institution is evaluating the staffing model of the internal audit activity (IAA). According to IIA guidance, which of the following are the most appropriate strategies to maximize the value of the current IAA resources?

• The annual audit plan should include audits that are consistent with the skills of the IAA.

• Audits of high-risk areas of the organization should be conducted by internal audit staff.

• External resources may be hired to provide subject-matter expertise but should be supervised.

• Auditors should develop their skills by being assigned to complex audits for learning opportunities.

An internal auditor is conducting an assessment of the purchasing department. She has worked the full amount of hours budgeted for the engagement; however, the audit objectives are not yet complete. According to IIA guidance, which of the following are appropriate options available to the chief audit executive?

1. Allow the auditor to decide whether to extend the audit engagement.

2. Determine whether the work already completed is sufficient to conclude the engagement.

3. Provide the auditor feedback on areas of improvement for future engagements.

4. Provide the auditor with instructions and directions to complete the audit.

Which of the following is a detective control for managing the risk of fraud?

Which of the following is the primary purpose of financial statement audit engagements?

Which of the following statements about internal audit's follow-up process is true?

A large retail organization, which sells most of its products online, experiences a computer hacking incident. The chief IT officer immediately investigates the incident and concludes that the attempt was not successful. The chief audit executive (CAE) learns of the attack in a casual conversation with an IT auditor. Which of the following actions should the CAE take?

1. Meet with the chief IT officer to discuss the report and control improvements that will be implemented as a result of the security breach, if any.

2. Immediately inform the chair of the audit committee of the security breach, because thus far only the chief IT officer is aware of the incident.

3. Meet with the IT auditor to develop an appropriate audit program to review the organization's Internet-based sales process and key controls.

4. Include the incident in the next quarterly report to the audit committee.

According to IIA guidance, which of the following is true regarding audit supervision?

1. Supervision should be performed throughout the planning, examination, evaluation, communication, and follow-up stages of the audit engagement.

2. Supervision should extend to training, time reporting, and expense control, as well as administrative matters.

3. Supervision should include review of engagement workpapers, with documented evidence of the review.

According to IIA guidance, which of the following statements is true regarding the authority of the chief audit executive (CAE) to release previous audit reports to outside parties?

A chief audit executive is preparing interview questions for the upcoming recruitment of a senior internal auditor. According to IIA guidance, which of the following attributes shows a candidate's ability to probe further when reviewing incidents that have the appearance of misbehavior?

During an audit of the accounts receivable (AR) process, an internal auditor noted that reconciliations are still not performed regularly by the AR staff, a recommendation that was made following a previous audit. Monitoring by the financial reporting function has failed to detect the shortcoming. Both the financial reporting function and AR report to the controller, who is responsible for implementing action plans. Which of the following supports the internal auditor's decision to combine both observations into one reported finding?

Which of the following is the most important concept to be included in a consulting engagement agreement?

Due to a recent system upgrade, an audit is planned to test the payroll process. Which of the following audit objectives would be most important to prevent fraud?

Which of the following would not be a typical activity for the chief audit executive to perform following an audit engagement?

An internal auditor and engagement client are deadlocked over the auditor's differing opinion with management on the adequacy of access controls for a major system. Which of the following strategies would be the most helpful in resolving this dispute?

After the team member who specialized in fraud investigations left the internal audit team, the chief audit executive decided to outsource fraud investigations to a third party service provider on an as needed basis. Which of the following is most likely to be a disadvantage of this outsourcing decision?

According to IIA guidance, which of the following factors should the auditor in charge consider when determining the resource requirements for an audit engagement?

According to IIA guidance,which of the following is true about the supervising internal auditor's review notes?

• They are discussed with management prior to finalizing the audit.

• They may be discarded after working papers are amended as appropriate.

• They are created by the auditor to support her fieldwork in case of questions.

• They are not required to support observations issued in the audit report.

Which of the following is the primary reason the chief audit executive should consider the organization's strategic plans when developing the annual audit plan?

Which of the following is not an outcome of control self-assessment?

Which of the following components should be included in an audit finding?

1. The scope of the audit.

2. The standard(s) used by the auditor to make the evaluation.

3. The engagement's objectives.

4. The factual evidence that the internal auditor found in the course of the examination.

According to IIA guidance, which of the following statements are true regarding the internal audit plan?

1. The audit plan is based on an assessment of risks to the organization.

2. The audit plan is designed to determine the effectiveness of the organization's risk management process.

3. The audit plan is developed by senior management of the organization.

4. The audit plan is aligned with the organization's goals.

Which of the following is an effective approach for internal auditors to take to improve collaboration with audit clients during an engagement?

1. Obtain control concerns from the client before the audit begins so the internal auditor can tailor the scope accordingly.

2. Discuss the engagement plan with the client so the client can understand the reasoning behind the approach.

3. Review test criteria and procedures where the client expresses concerns about the type of tests to be conducted.

4. Provide all observations at the end of the audit to ensure the client is in agreement with the facts before publishing the report.

The external auditor has identified a number of production process control deficiencies involving several departments. As a result, senior management has asked the internal audit activity to complete internal control training for all related staff. According to IIA guidance, which of the following would be the most appropriate course of action for the chief audit executive to follow?

According to IIA guidance, which of the following procedures would be least effective in managing the risk of payroll fraud?

Which of the following activities should the chief audit executive perform to ensure compliance with an organization's code of conduct?

Which of the following factors have the greatest influence on the independence of the internal audit activity?

Which of the following is an example of a directive control?

An organization is facing a financial downturn and needs to impose major budget reductions to all departments. According to MA guidance, which of the following actions is most appropriate for the board to take to evaluate the potential impact on the internal audit activity?

Which of the following are core responsibilities to be included in the internal audit charter?

1. Review reliability and integrity of financial and operating information and the means used to identify, measure, classify, and report such information.

2. Determine the adequacy and effectiveness of the organization’s systems of internal accounting and operating controls.

3. Participate in the planning and performance of audits of potential acquisitions with the organization's outside accountants and other members of the corporate staff.

4. Report to those members of management who should be informed of results of audit examinations, the audit opinions formed, and the recommendations made.

The chief audit executive (CAE) of a small internal audit activity (IAA) performs all high-risk engagements on the annual audit plan to make use of his knowledge and experience and to maximize the efficient use of audit resources. Which of the following statements is most relevant regarding this practice?

Reviewing prior audit reports and supporting workpapers before an engagement starts enables an internal auditor to do which of the following?

1. To understand better the activity and processes that will be audited.

2. To identify the audit procedures that will be used during the engagement.

3. To ensure that matters of greatest vulnerability will be addressed.

4. To use the information obtained as evidence in the current engagement.

According to COSO, which of the following describes a principle related to the control environment?

Which of the following is not an objective of internal control?

An auditor in charge was reviewing the workpapers submitted by a newly hired internal auditor. She noted that the new auditor's analytical work did not include any rating or quantification of the risk assessment results, and she returned the workpapers for correction. Which section of the workpapers will the new auditor need to modify?

An internal audit charter should do which of the following?

Faced with a complex, highly technical construction audit engagement, the chief audit executive (CAE) considered complementing the current internal audit resources by engaging the services of a civil engineer.

Which of the following should the CAE consider in determining whether the engineer possesses the necessary skills to perform the engagement?

1. Professional certification, license, or other recognition of the engineer's competence in the relevant discipline.

2. Experience of the engineer in the type of work being considered.

3. Compensation or other incentives that the engineer may receive.

4. The extent of other ongoing services that the engineer may be performing for the organization.

During an audit engagement, the internal auditor discussed a risk mitigation recommendation with the manager of the area under review. The manager disagreed with the risk assessment and recommendation. The two failed to come up with an alternative solution, and the auditor decided to proceed with including the original recommendation in the engagement report. Which of the following is especially important in dealing with this type of situation?

If appropriate safeguards exist, which of the following is considered a legitimate internal audit role within risk management at an organization?

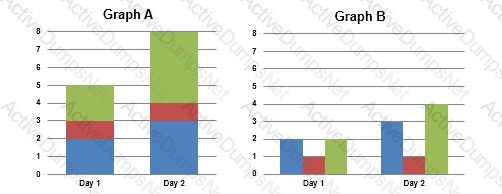

Click the Exhibit.

Internal auditors are asked to keep track of how many hours per day they spend planning the audit, conducting the engagement, and writing the audit report. The data for two days has been collected as follows:

Day 1

Day 2

Planning the audit

2 hours

3 hours

Conducting the engagement

1 hour

1 hour

Writing the audit report

2 hours

4 hours

Which of the following graphs depicts the data accurately?

According to IIA guidance, which of the following statements is true when an internal auditor performs consulting services that improve an organization's operations?

A chief audit executive (CAE) is selecting an internal audit team to perform an audit engagement that requires a high level of knowledge in the areas of finance, investment portfolio management, and taxation. If neither the CAE nor the existing internal audit staff possess the required knowledge, which of the following actions should the CAE take?

According to IIA guidance, which of the following describes the primary reason to implement environmental and social safeguards within an organization?

Which of the following controls could an internal auditor reasonably conclude is effective by observing the physical controls of a large server room?

An organization invests its savings in a volatile stock with the potential for high gains rather than a mutual fund with a lower expected return and lower volatility. This best describes which of the following risk concepts?

While preparing for an audit of senior management expenses, the chief audit executive (CAE) learns that management is unable to locate a number of original expense claims to support the related disbursements. She decides to defer the engagement until they can be located. Which of the following principles likely guided the CAE's decision?

Which of the following techniques would provide the most compelling evidence that a safety hazard exists within a manufacturing facility?

An internal auditor is evaluating techniques management uses to mitigate risks within a particular product division. Which of the following is an example of risk reduction?

Which of the following professional development approaches would offer internal auditors the most opportunities to broaden their engagement experiences?

Which of the following enhances the independence of the internal audit activity?

According to IIA guidance, when preparing the charter for the internal audit activity, the chief audit executive (CAE), board, and senior management should agree on which of the following?

1. The standards to be used by the internal audit activity.

2. The internal audit activity's code of ethics.

3. The CAE's reporting line.

4. The internal audit activity's responsibilities.

According to The IIA's Code of Ethics, which of the following is true?

A government agency maintains a system of internal control, according to the COSO model, and has made a change to its employee performance reviews and rewards program. This change relates to which of the following components of COSO's internal control framework?

Which of the following is the primary engagement responsibility of an entry-level internal auditor?

Which of the following documents is most appropriate in promoting the objectivity of the internal audit activity?