CIMA F2 F2 Advanced Financial Reporting Exam Practice Test

F2 Advanced Financial Reporting Questions and Answers

The consolidated statement of profit or loss for VW for the year ended 30 September 20X7 includes the following:

What is VW's interest cover for the year ended 30 September 20X7?

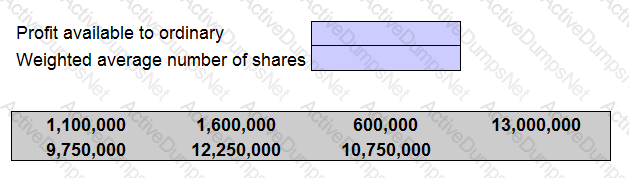

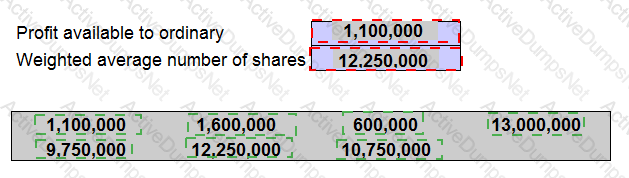

On 1 January 20X6 AB, a listed entity, had 10,000,000 $1 ordinary shares in issue. On 1 April 20X6 AB issued 3,000,000 $1 ordinary shares at their full market price. AB's profit was reported as $1,100,000 after charging corporate income tax of $500,000.

Place the correct values for profit and weighted average number of shares in the boxes below that will be used to calculate AB's earnings per share for the year to 31 December 20X6.

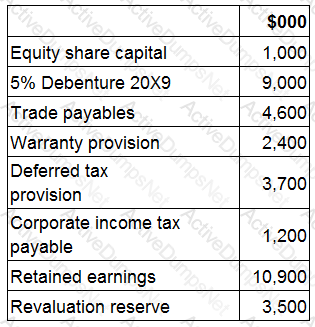

Information from the financial statements of an entity for the year to 31 December 20X5:

The gearing ratio calculated as debt/equity and interest cover are:

Which of the following reduce the usefulness of ratio analysis when comparing entities that operate in the same industry? Select ALL that apply.

The dividend yield of ST has fallen in the year to 31 May 20X5, compared to the previous year.

The share price on 31 May 20X4 was $4.50 and on 31 May 20X5 was $4.00. There were no issues of share capital during the year.

Which of the following should explain the reduction in the dividend yield for the year to 31 May 20X5 compared to the previous year?

AB sold the majority of its operating equipment to LM for cash on 30 December 20X9 and then immediately leased it back under an operating lease.

AB used the cash proceeds from the sale to reduce its long term borrowings significantly. No early repayment charge was levied by the lender.

Which of the following statements is true in respect of AB's ratios calculated at 31 December 20X9?

EF obtained a government licence, free of charge, to operate a silver mine in 20X7 and $5 million was spent on preparing the site. The mine commenced operation on 1 January 20X8. The licence requires that at the end of the mine's useful life of 20 years, the site above ground must be reinstated to its original position.

EF estimated that the cost in 20 years' time of this reinstatement will be $3 million, which has a present value of $1 million at 1 January 20X8.

Which THREE of the following describe how the cost of the reinstatement of the site should be treated in the financial statements of EF in the year ended 31 December 20X8?

Which of the following statements are true regarding consolidated cash flows after the acquisition of a subsidiary?

Select ALL that apply.

RST sells computer equipment and prepares its financial statements to 31 December.

On 30 September 20X5 RST sold computer software along with a two year maintenance package to a customer. The customer is given the right to return the goods within six months and claim a full refund if they are not satisfied with the computer software. The risk of return is considered to be insignificant for RST.

How should the revenue from this transaction and the right of return be recognised in the financial statements for the year ended 31 December 20X5?

Which of the following is NOT an example of an unconsolidated structured entity as defined in IFRS12 Disclosure of Interests in Other Entities?

EF has redeemable 10% bonds which are currently trading at $94.00 for each $100 of nominal value. The bonds can be redeemed at par in five years' time. The corporate income tax rate is 22%.

The present value of the cash flows associated with $100 nominal value of these bonds at a discount rate of 7% is $9.28.

Calculate the post tax cost of debt.

Give your answer as a percentage to one decimal place.

%

If you were asked to express the overall performance of an entity as a percentage of its total investment in net assets which of the following ratios would you calculate?

AB acquired an investment in a debt instrument on 1 January 20X5 at its nominal value of $25,000, which it intends to hold until maturity. The instrument carried a fixed coupon interest rate of 5%, payable in arrears. Transactions costs of $5,000 were paid in respect of this investment. The effective interest rate applicable to this instrument was estimated at 9%.

Calculate the value of this investment that AB will include in its statement of financial position at 31 December 20X5.

Give your answer to the nearest whole number.

$ ?

AB owned 80% of the equity share capital of FG at 1 January 20X6. AB disposed of 10% of FG's equity share capital on 31 December 20X6 for $400,000. The non controlling interest was measured at $700,000 immediately prior to the disposal.

Which of the following represents the adjustment that AB made to non controlling interest in respect of the disposal when it prepared its consolidated financial statements at 31 December 20X6?

ST acquired 75% of the 2 million $1 equity shares of CD on 1 January 20X3, when the retained earnings of CD were S3,550,000. CD has no other reserves.

ST paid $5,600,000 for the shares in CD and the non controlling interest was measured at its fair value of S1,400,000 at acquisition.

At 1 January 20X3, the fair value of CD's net assets were equal to their carrying amount, with the exception of a building. This building had a fair value of $1,000,000 in excess of its carrying amount and a remaining useful life of 25 years on 1 January 20X3.

At 31 December 20X5, the retained earnings of ST and CD were $8,500,000 and $5,250,000 respectively.

What is the value of retained earnings that will be presented in the consolidated statement of financial position of ST as at 31 December 20X5?

Which of the following is a related party according to the definition of a related party in IAS24 Related Party Disclosures?

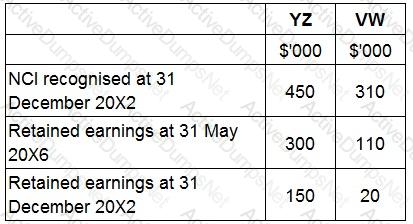

AB acquired 90% of the equity of YZ on 31 December 20X2. On the same date YZ acquired 60% of the equity shares of VW for $750,000. AB has no other subsidiaries.

The following information regarding YZ and VW was available:

What amount will AB include in its consolidated statement of financial position in respect of non controlling interest at 31 May 20X6?

CD granted 1,000 share options to its 100 employees on 1 January 20X8.To be eligible, employees must remain employed for 3 years from the grant date. In the year to 31 December 20X8, 15 staff left and a further 25 were expected to leave over the following two years.

The fair value of each option at 1 January 20X8 was $10 and at 31 December 20X8 was $15.

Which THREE of the following are true in respect of recording these share options in the year ended 31 December 20X8?

AB acquired its one subsidiary, CD, on 1 January 20X1. At this date the fair value of CD's property, plant and equipment was found to be $40 million higher than its carrying value. The relevant items had a remaining estimated useful life of 10 years from the date of acquisition.

At 31 December 20X4 AB and CD presented property, plant and equipment of $100 million and $50 million respectively in their individual financial statements.

The value of property, plant and equipment presented in AB's consolidated statement of financial position at 31 December 20X4 is:

What is the total comprehensive income attributable to the non-controlling interest that will be presented in GHI's consolidated statement of changes in equity for the year ended 31 December 20X4?

GH's financial statements show the following:

What is the value of the dividend received from the associate to be included in GH's consolidated statement of cash flows for the year?

Give your answer to the nearest $000.

$ ? 000

CD reported a balance of $3,000,000 for property, plant and equipment in its individual financial statements at 31 December 20X8.

Calculate the value of the property, plant and equipment that will be included in CD's consolidated statement of financial position.

Give your answer to the nearest $000.

$? 000

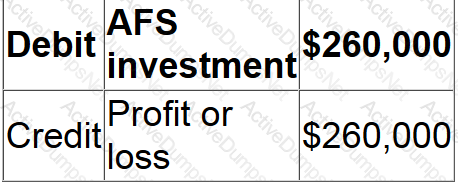

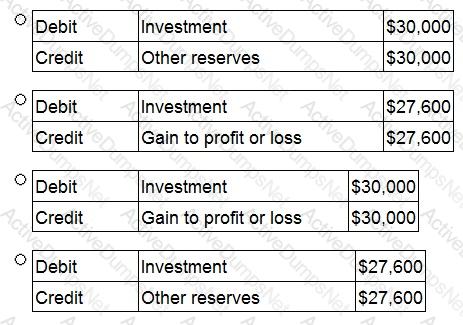

KL acquired 2 million $1 equity shares in MN on 18 July 20X0 for $1.65 a share and classified this investment as available for sale (AFS) in accordance with IAS 39 Financial instruments: Recognition and Measurement.

KL paid a 0.5% transaction fee to its broker on this transaction. MN's shares were trading at $1.78 on 31 December 20X0.

Which of the following journals records the subsequent measurement of this investment at 31 December 20X0?

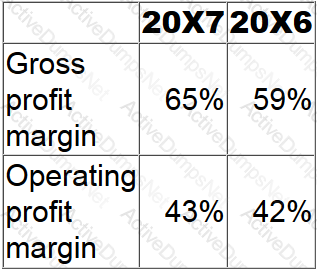

Ratios calculated from the financial statements of ST Group for the years ended 31 August 20X7 and 20X6 are as follows:

Which of the following would have contributed to the movements in these ratios?

On 1 September 20X3, GH purchased 200,000 $1 equity shares in QR for $1.20 each and classified this investment as held for trading.

GH paid a 1% transaction fee to its broker on this transaction. QR's equity shares had a fair value of $1.35 each on 31 December 20X3.

Which of the following journals records the subsequent measurement of this financial instrument at 31 December 20X3?

JJ's current share price is $1.80, with a dividend of $0.20 a share just about to be paid.

Dividends have increased at an average annual growth rate of 4.5% and this is expected to continue into the future.

What is JJ's cost of equity?

ST has sold its main office property, which had a carrying value of $360,000, to AB, a property management entity.

The property was sold for $400,000 which is equal to its fair value and was immediately leased back under an operating lease agreement.

Which of the following journals will record this transaction?

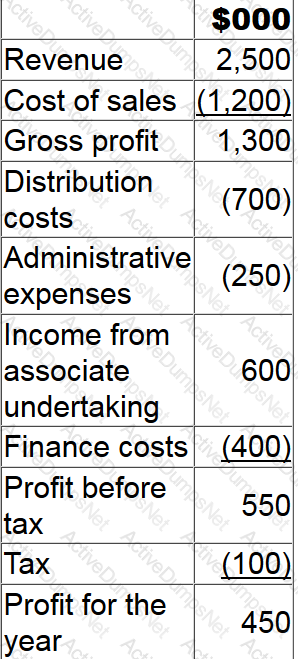

FG's statement of profit or loss account for year ended 31 December 20X1 is:

What is the operating profit margin for FG for the year ended 31 December 20X1?

Give your answer to the nearest whole %.

? %

Which of the following statements is true in respect of ST's gross profit margin based on the information given?

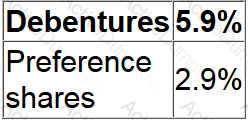

UV has raised $100,000 through the issue of two irredeemable financial instruments:

• 6% debentures with a current market value of $101.50 per $100 nominal value; and

• 8% preference shares with a current share price of $2.20 each.

The corporate income tax rate is 20%

What is the post tax cost of debt for each of these instruments?

A )

Which of the following is the correct calculation for basic earnings per share in accordance with IAS 33 Earnings Per Share?

Information extracted from JK's statement of financial position for the year ended 31 May 20X5 is as follows:

Calculate the gearing ratio (Debt/Equity measured as a percentage) at 31 May 20X5.

Give your answer to one decimal place.

? %

Which of the following is a related party according to the definition of a related party in IAS24 Related Party Disclosures?

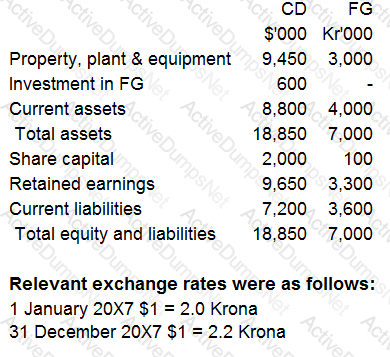

CD acquired 100% of the equity share capital of FG for cash consideration of Kr1,200,000 on 1 January 20X7.

Retained earnings of FG at the date of acquisition was Kr800,000. CD operates from Country A and its functional and presentation currency is $. FG is located and trades throughout Country B and its functional currency is the Krona (Kr).

CD has no other subsidiaries. Goodwill had not suffered any impairment to date.

Summarised data from the statements of financial position for both entities at 31 December 20X7 is presented below:

Calculate the exchange difference arising on the retranslation of goodwill on the acquisition in the consolidated statement of financial position of CD at 31 December 20X7.

Give your answer to the nearest $000.

On 1 January 20X4 JK had 1,500,000 ordinary shares in issue. On 1 September 20X4 JK issued 600,000 ordinary shares at the market value of $2.50 a share. For the financial year ended 31 December 20X4 the statement of profit or loss shows profit before tax of $625,000 and profit after tax of $500,000.

What is the earnings per share for the year ended 31 December 20X4?

XY puchased 2% of the equity shares of FG on 1 October 20X3.

XY paid $25,000 for the shares as well as a transaction cost of 2.5% of the purchase price.

The shares are being held for short term trading and XY intend to sell them in December 20X3.

At the year end of 31 October 20X3, the shares in FG could be sold for $28,000.

What is the journal entry to record the subsequent measurement for this investment at 31 October 20X3?

When preparing a consolidated statement of cash flows, which of the following describes the correct presentation of an associate's dividends?

Which of the following examples of contracts will use cost of sales as the balancing figure when calculating profit or loss?

Select ALL that apply.

Which THREE of the following statements are true in relation to financial assets designated as fair value through profit or loss under IAS 39 Financial Instruments: Recognition and Measurement?

GG's gearing is currently 50% compared to the industry average of 40% (both measured as debt/equity). GG's debt is all in the form of a single bank loan that is repayable in five years' time. The directors of GG are seeking to raise finance for a new project and they are considering an additional bank loan from the same bank.

Which of the following would prevent the bank from lending the finance for the project in the form of a new bank loan?