CIMA F1 Financial Reporting Exam Practice Test

Financial Reporting Questions and Answers

UV's financial statements for the year ended 31 March 20X8 were approved for publication on 30 June 20X8.

In accordance with IAS 10 Events After the Reporting Period, which of the following material events would have been classified as a non-adjusting event in these financial statements?

According to IAS 21 The Effects of Changes in Foreign Exchange Rates, an entity should determine its functional currency.

Which of the following is NOT a factor that should be considered by an entity when determining its functional currency?

Which of the following is NOT a responsibility of the International Accounting Standards Board?

The external auditors have completed their audit and have discovered a material but not pervasive error in the financial statements of JK.

The directors of JK have refused to change the financial statements.

What type of modified audit report should be issued?

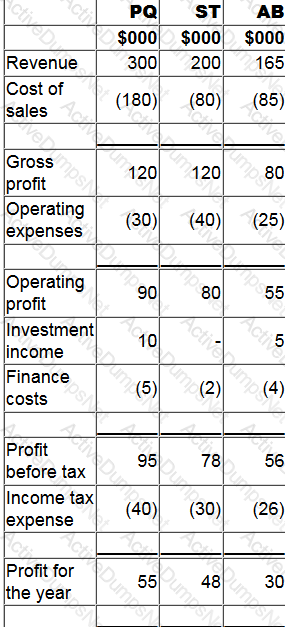

The statement of profit or loss for PQ, ST and AB for the year ended 31 December 20X0 are shown below:

1. PQ acquired 80% of its subsidiary, ST, on 1 January 20X0 and 40% of its associate, AB, on 1 September 20X0.

2. Since acquistion PQ has sold goods to ST and AB for $20,000 and $30,000 respectively. At the year end both ST and AB have 50% of these goods remaining in inventory. PQ uses a mark-up of 20% on all of its sales.

3. Since acquisition the goodwill in respect of ST has been impaired by $8,000 and the investment in AB has been impaired by $2,000.

4. PQ uses the fair value method for non-controlling interest at acquisition.

Calculate the profit attributable to the non-controlling interests disclosed in PQ's consolidated statement of profit or loss for the year ended 31 December 20X0.

Give your answer to the nearest whole $.

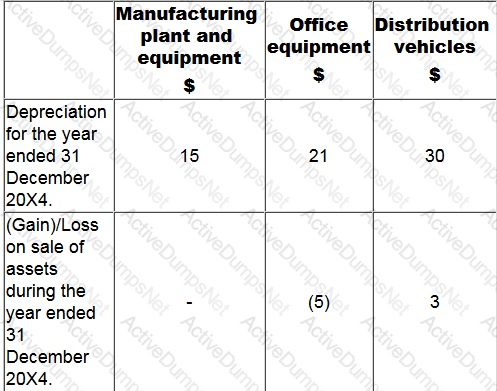

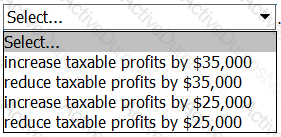

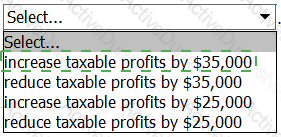

KL has S90.000 of plant and machinery which was acquired on 1 June 20X4. Tax depreciation rates on plant and machinery are 20% reducing balance. All plant and machinery was sold for 560,000 on 1 June 20X6

Calculate the tax balancing allowance or charge on disposal tor the year ended 31 May 20X7 and state the effect on the taxable profit.

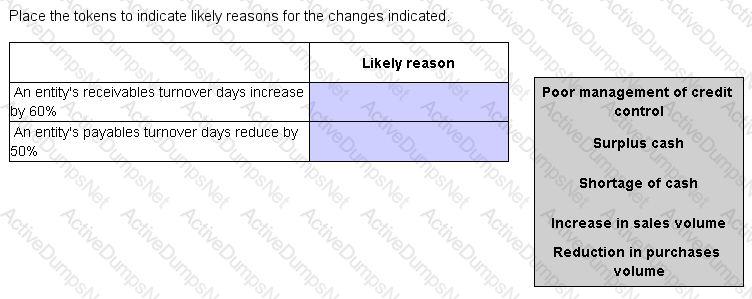

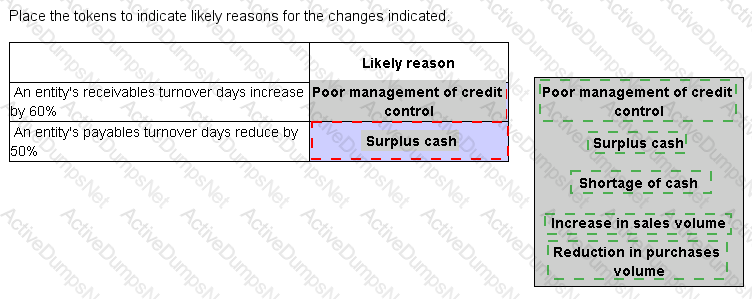

Which THREE of the following matters should an entity consider when determining the credit terms granted to a customer?

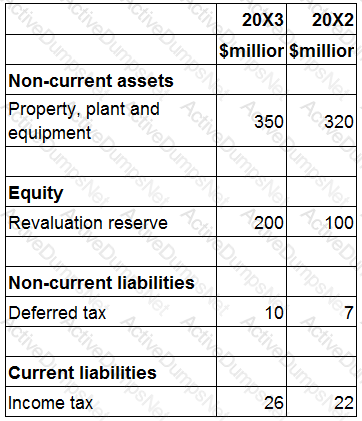

The following information is extracted from the statement of financial position for ZZ at 31 March 20X3:

Included within cost of sales in the statement of profit or loss for the year ended 31 March 20X3 is $20 million relating to the loss on the sale of plant and equipment which had cost $100 million in June 20X1.

Depreciation is charged on all plant and equipment at 25% on a straight line basis with a full year's depreciation charged in the year of acquisition and none in the year of sale.

The revaluation reserve relates to the revaluation of ZZ's property.

The total depreciation charge for property, plant and equipment in ZZ's statement of profit of loss for the year ended 31 March 20X3 is $80 million.

The corporate income tax expense in ZZ's statement of profit or loss for year ended 31 March 20X3 is $28 million.

ZZ is preparing its statement of cash flows for the year ended 31 March 20X3.

What figure should be included within cash flows from investing activities for the proceeds of sale of plant and equipment?

An entity purchased an asset on 1 April 20X4 for $320,000, exclusive of import duties of $32,000.

The entity sold the asset on 31 March 20X9 for $480,000 incurring legal fees of $12,000.

The entity is resident in Country Y where chargeable capital gains are taxed at 20% and no indexation is allowed.

Calculate the amount of capital tax that the entity is due to pay.

Give your answer to the nearest whole $.

FG purchased 40% of the equity shares of QR and exerted significant influence over the board of the directors.

QR will be classified as____of FG.

The following information relates to AA.

Extract of Trial Balance at 31 December 20X4;

Notes

(i) Inventory at 31 December 20X4 was valued at cost at $30.

(ii) The loan which was received on 1 July 20X4 is repayable in 20X9.

(iii) Corporate income tax represents an over-provision of tax for the year ended 31 December 20X3. AA reported a loss for tax purposes for the year ended 31 December 20X4 and a tax refund is expected amounting to $20.

(iv) Cost of sales, administration and distribution costs need to be adjusted for the following:

Calculate gross profit for the year ended 31 December 20X4.

Give your answer as a whole $.

Which of the following is correct?

The primary purpose of a cash budget prepared on a monthly basis is to determine:

Which THREE of the following are potential implications to a manufacturing business of holding insufficient inventory of raw materials?

BBB has been experiencing liquidity problems and currently has an overdraft with the bank.

Which THREE of the following would be appropriate measures to help address this problem?

AB sells to ST, a group entity, 10,000 units at $2.50 each. The market value was $6 each.

The effect on AB of the transfer pricing legislation on this transaction would be to: .

In accordance with IFRS 3 Business Combinations, acquisition accounting of an investment in another entity within the consolidated statement of financial position means that the:

HI commenced business on 1 April 20X3. Sales in April 20X3 were $30,000. This is forecast to increase by 2% per month.

Credit sales accounted for 50% of sales. Credit sales customers are allowed one month to pay; 75% of April credit customers paid on time. A further 20% are expected to pay after more than one month, but before two months. The remaining 5% are not expected to pay. All these percentages are expected to continue in the near future.

Calculate the total amount of cash HI should forecast to be received in June 20X3.

Give your answer to the nearest whole $.

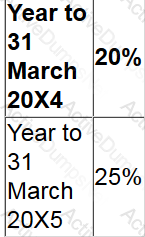

The accounting profit before tax of an entity was $243,200 for the year ended 31 July 20X4.

The accounting profit included disallowable income from government grants of $48,000 and disallowable expenditure of $25,600 on entertaining expenses.

The entity also paid a $40,000 dividend to shareholders. The tax rates for the country were as follows:

Calculate the tax the entity is due to pay for the year ending 31 July 20X4.

Which of the following would be capitalized as an intangible asset in accordance with IAS 38 Intangible Assets?

OP holds an investment property purchased on 1 January 20X3 for $700,000 with a useful economic life of 25 years.

At 31 December 20X5 the fair value of the investment property was $750,000 with a revised useful economic life of 25 years from that date.

OP has been carrying the investment property using the cost model until 31 December 20X5.

The directors wish to change their valuation method to fair value in accordance with IAS 40 Investment Property.

Which of the following is the correct treatment of the revaluation gain and the value of the property in the statement of financial position at 31 December 20X5?

The following information is extracted from QQ's statement of financial position at 31 March:

Included in other payables is interest payable of $80,000 at 31 March 20X2 and $73,000 at 31 March 20X1.

The following information if included within QQ's statement of profit or loss for the year ended 31 March 20X2.

Included within finance cost is $124,000 which relates to interest paid on a finance lease. QQ includes finance lease interest within financing activities on its statement of cash flows.

What cash outflow figure should be included as interest paid within the net cash flow from operating activities for QQ for the year ended 20X2?

Give your answer to the nearest $000.

STU has a non-current asset which originally cost $250,000, has an expected life of 8 years and an estimated residual value of $25,000. The asset is depreciated at 25% a year on a reducing balance basis On 1 July 20X5 the accumulated depreciation for this asset is $109,375

What is the depreciation charge for the year ending 30 June 20X6?

Give your answer to the nearest whole number.

Select THREE actions that should be taken by a business offering credit to its customers to ensure that amounts owing are collected as quickly as possible.

PP supplies zero-rated and standard-rated goods. During the year ended 30 March 20X3, the standard-rated goods made up 50% of the total supplies. During the year ended 30 March 20X4 this percentage increased to 60%.

What percentage of input tax suffered can PP claim back in the year ended 30 March 20X4?

Give your answer as a whole number.

The following information relates to a single asset:

*Original cost of $186,000

*Estimated residual value of $6,000

*Expected useful life of 10 years

*Accumulated depreciation at 31 December 20X5 of $66,960

*Annual depreciation rate of 20% on a reducing balance basis

Calculate the amount of depreciation that should be charged to profit or loss for the year ended 31 December 20X6.

Give your answer to the nearest whole number.

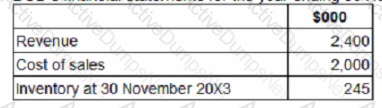

BCD's financial statements for the year ending 30 November 20X3 include the following:

Inventory at 30 November 20X2 was $220,000.

What is BCD's average inventory holding period for the year ended 30 November 20X3?

An asset cost $250,000 on 1 January 20X1 and on that date was assessed to have a residual value of $40,000 and a useful economic life of six years. On 1 January 20X4 management assessed that the remaining useful economic life of the asset was five years and that the asset had a residual value of nil.

What is the depreciation charge for this asset in the year ended 31 December 20X4?

Give your answer to the nearest whole number.

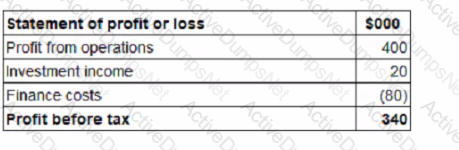

Below are extracts from LLL's financial statements for the year ended 31 December 20X2.

Depreciation of $25,000 was charged on properly, plant and equipment in the year and there were no disposals

What is the cash generated from operations for inclusion in LLL's statement of cash flows for the year ended 31 December 20X2?

In accordance with The Conceptual Framework for Financial Reporting, faithful representation is a fundamental qualitative characteristic.

To be a faithful representation financial information must be as far as possible which THREE of the following?

The tax rules in a country state that all tax returns must be filed by 31 March each year and that any outstanding tax balance must be paid by 14 April each year. An entity filed its tax return on 10 April 20X2 and paid the outstanding tax on 20 April 20X2.

Which TWO of the following powers is the tax authority likely to have in respect of these actions by the entity?

What does the exemption method of giving double taxation relief mean?

In most developed countries employers deduct the tax from employees' pay each month and then pay the tax to the tax authorities on behalf of the employee on a monthly basis.

Which THREE of the following are advantages of this system to the employee?

The IV Group is formed of I Ltd and its subsidiary company V Ltd. I Ltd purchased 67% of V Ltd's ordinary share capital on 31 March 20X3.

The purchase cost I Ltd £129,000. At the date of purchase V Ltd's net assets were £155,000 while its share capital was £37,000. NCI fair value on the date of acquisition was £31,000.

What was the amount of goodwill I Ltd paid as part of the acquisition. Calculate this figure using both the proportion of net assets method and the full good will method for valuing the non-controlling interest.

Country J is a newly formed independent country and it's accounting professionals are considering adopting international financial reporting standards (IFRS).

Which of the following is a disadvantage to Country J of adopting IFRS as their local generally accepted accounting practice (GAAP)?

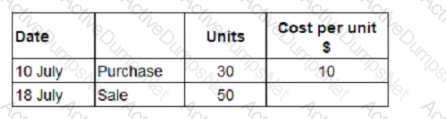

On 1 July 20X8 JKL has 100 units of inventory, which cost $8 each. The following transactions arose during the month of July:

JKL values inventory using the first in. first out method.

What is the value of JKL's inventory at 31 July 20X8?

Give your answer to the nearest $.

Corporate governance is the means by which an entity is operated and

Mr K is being pressured by his manager to change figures in his report so that it will improve his manager's bonus.

His manager has promised Mr K a promotion if he agrees to do this.

What threats is Mr K facing?

Which of the following is the main purpose of corporate governance regulation?

While conducting their audit, auditor 0 did not encounter issues which significantly limited the scope of their audit, however they did run into problems in that they disagreed with the management on facts in the

statements.

These disagreements were somewhat material, but they did not affect the auditor's overall opinion of the business. Which of the following statements should auditor 0 issue?

Which TWO of the following are features of a bank overdraft?

Which THREE of the following are costs that a business might incur as a result of holding insufficient inventory of raw materials?

XY is an entity incorporated in Country B but operates in several countries. Monthly management meetings to decide on strategic matters take place in Country A, where the majority of its production happens. XY sells most of its goods to Country C.

In accordance with the Organization for Economic Co-operation and Development (OECD) rules on corporate residence which of the following statements is true?

An entity has an inventory holding period of 52 days.

This means that the inventory:

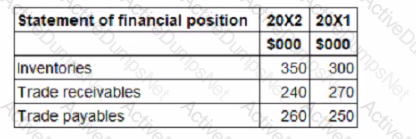

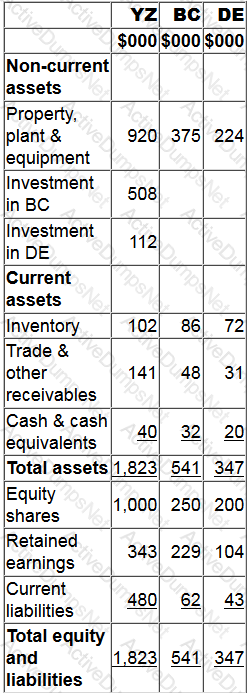

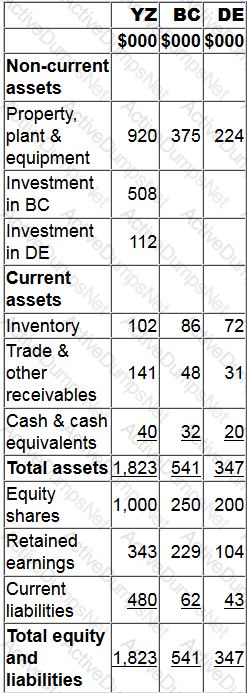

Statements of financial position for YZ, BC and DE at 31 March 20X2 include the following balances:

YZ purchased 90% of BC's equity shares for $508,000 on 1 January 20X2. On 1 January 20X2 BC's retained earnings were $183,000. YZ uses the proportion of net assets method to value non-controlling interest at acquisition.

YZ purchased 30% of DE's equity shares on 1 April 20X1 for $112,000. DE's retained earnings at 1 April 20X1 were $88,000.

On 1 February 20X2 YZ sold goods to BC for $28,000 at a mark up of 25% on cost. All the goods were still in BC's inventory at 31 March 20X2.

Calculate the amount of the non-controlling interest to be included in YZ's consolidated statement of financial position at 31 March 20X2.

Give your answer to the nearest whole $.

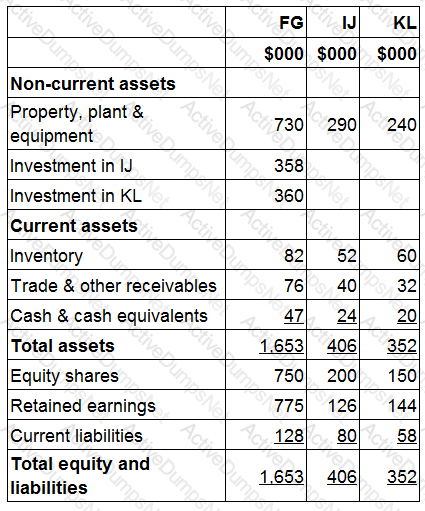

Statements of financial position for FG, IJ and KL at 31 December 20X5 include the following balances:

FG acquired 90% of IJ's equity shares for $358,000 on 1 July 20X5 when IJ's retained earnings were $98,000.

FG acquired 100% of KL's equity shares for $360,000 on 1 January 20X5 when KL's retained earnings were $155,000.

FG used the proportion of net assets method to value non-controlling interests at acquisition.

KL sold a piece of land to FG for $130,000 on 1 September 20X5. At the date of transfer the land had a carrying value of $50,000.

The management of FG expect KL to make profits in the future and no impairment ot its goodwill was proposed at 31 December 20X5.

Calculate the value of property, plant and equipment to be recognized in FG's consolidated statement of financial position at 31 December 20X5.

Give your answer to the nearest whole $.

On 1 July 20X7, VWX enters into a 12-month lease for personal computers paying a non-refundable deposit of $600. Lease payments of $500 are paid monthly in arrears. VWX chooses to recognise the assets in the lease as short life and low value

Which of the following gives the correct value for the expense in the statement of profit or loss and corresponding prepayment and accrual in VWX's statement of financial position for the year ended 31 December 20X7?

A

B

C

D

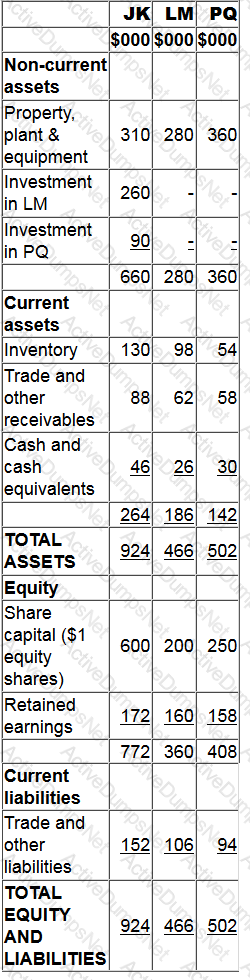

Statements of financial position as at 31 December 20X8 for JK, LM and PQ are as follows:

[1] JK purchased 80% of LM's $1 equity shares on 1 January 20X8 for $260,000 when the retained earnings of JK were $110,000. At that date the non-controlling interest had a fair value of $63,000.

[2] JK purchased 25% of PQ's $1 equity shares on 1 January 20X8 for $90,000 when the retained earnings of PQ were $96,000.

[3] During the year JK sold goods to LM for $32,000 at a mark up of 33.33% on cost. Half of the goods were still in LM's inventory at 31 December 20X8.

[4] LM transferred $32,000 to JK on 30 December 20X8 in settlement of the inter-group trade. JK did not record the cash in its financial records until 2 January 20X9.

Calculate the goodwill arising on the acquisition LM.

Give your answer to the nearest $.

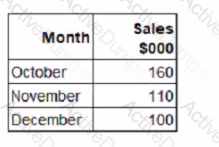

XYZ has the following data relating to the forecast sale of goods for the quarter to 31 December 20X2:

XYZ expects trade receivables to be settled as follows:

• 20% in the month of sale, by offering a settlement discount of 5%;

• 30% in the month following sale, and

• the remainder, after allowing for irrecoverable debts, in the subsequent month

$10,000 of the sales made in October 20X2 are expected to be irrecoverable

What is the forecast amount to be received by XYZ from trade receivables in December 20X2?

MNO is a commercial bank. One of MNO's clients is FGH, a trading company which sells goods to PQR.

MNO is asked to draw up an instrument between FGH and PQR in respect of goods sold FGH then asks MNO to sell this instrument on its behalf in the discount market MNO does this and pays the proceeds to FGH.

What source of short-term finance is being described here?

What is the correct classification of a 90-day government bond?

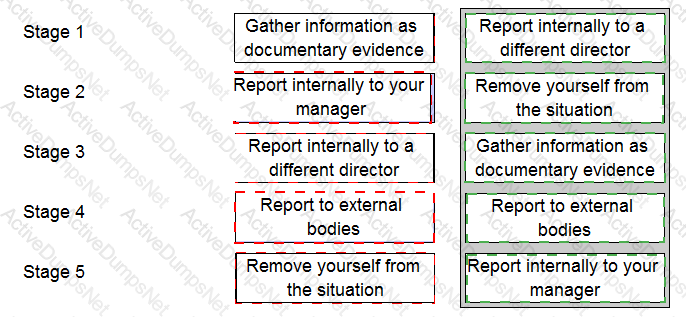

You work in the finance department of an entity. A director has approached you and asked you to falsify sales invoices which would significantly inflate revenue. The CIMA Code of Ethics suggests that you should deal with such an ethical dilemma by following a number of stages.

Place each of the stages identified below into chronological order.

Which of the following would NOT be a risk or impact of overtrading?

Which of the following is a characteristic of a defined contribution post-employment benefit scheme?

Which of the following would be found under the heading "other comprehensive income" in the statement of total comprehensive income?

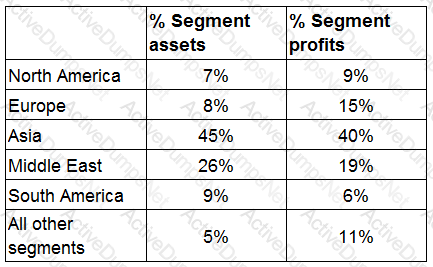

OP has five main geographic segments and reports segmental information in accordance with IFRS 8 Operating Segments.

Which THREE of the following would be regarded as operating segments of OP in accordance with IFRS 8?

LM is preparing its cash forecast for the next three months.

Which of the following items should be left out of its calculations?

Which of the following is a feature of value added tax (VAT)?

Statements of financial position for YZ, BC and DE at 31 March 20X2 include the following balances:

YZ purchased 90% of BC's equity shares for $508,000 on 1 January 20X2. On 1 January 20X2 BC's retained earnings were $183,000. YZ uses the proportion of net assets method to value non-controlling interest at acquisition.

YZ purchased 30% of DE's equity shares on 1 April 20X1 for $112,000. DE's retained earnings at 1 April 20X1 were $88,000.

On 1 February 20X2 YZ sold goods to BC for $28,000 at a mark up of 25% on cost. All the goods were still in BC's inventory at 31 March 20X2.

Calculate the value of inventory that will be included in YZ's consolidated statement of financial position at 31 March 20X2.

Give your answer to the nearest whole $.

Which of the following would NOT be considered an element of a regulatory framework for financial reporting?

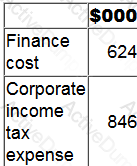

An entity had a current tax liability of $187,000 in its statement of financial position as at 30 September 20X5. It was subsequently negotiated and eventually agreed with the tax authorities that the entity would pay $192,000 and this was paid on 6 January 20X6.

The entity's management estimate that the tax due on profits for the year to 30 September 20X6 is $231,000.

Calculate the entity's corporate income tax expense included in its statement of profit or loss for the year ended 30 September 20X6.

Give your answer to the nearest whole $000.

For an incorporated business, the taxation of trading income is a form of direct taxation which is based on:

Which of the following does the phrase 'events after the reporting period' refer to?

Which of the following is NOT a feature of a multi-stage sales tax?

UK purchased an asset, with a useful economic life of 10 years, on 1 January 20X5 for $40,000. The asset was revalued on 31 December 20X6 to 544,000 and the directors believed its total useful economic life remained unchanged On 31 December 20X7 UK sells the asset for $50,000

How much will be recorded as a profit on disposal of the asset in UK's statement of profit or loss for the year ended 31 December 20X7?

Give your answer to the nearest $.

There are two main approaches to corporate governance: rules-based and principle-based.

Which THREE of the following are correct?

What does the tax credit method of giving double taxation relief mean?

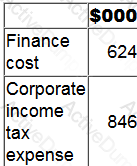

The following information is extracted from QQ's statement of financial position at 31 March:

Included in other payables is interest payable of $80,000 at 31 March 20X2 and $73,000 at 31 March 20X1.

The following information if included within QQ's statement of profit or loss for the year ended 31 March 20X2.

Included within finance cost is $124,000 which relates to interest paid on a finance lease. QQ includes finance lease interest within financing activities on its statement of cash flows.

QQ is preparing its statement of cash flows for the year ended 31 March 20X2.

What cash outflow figure should be included for corporate income tax paid within the cash flow from operating activities section of the statement?

Give your answer to the nearest $000.

A specialized product was commissioned by a customer and the agreed price was $38,000. The product was completed at a cost of $34,000.

It was then discovered that new regulations meant that the specialized product now failed health and safety requirements. The specialized product had to be modified to meet the new regulations at a cost of $9,000. The customer agreed to pay an extra $3,000 towards the modifications.

At 31 December 20X5 the specialized product was still in inventory and had not been modified.

Calculate the value of the specialized product that should be included in inventory as at 31 December 20X5.

Give your answer to the nearest whole $000.

Which of the following would NOT be assessed for tax under a Pay-As-You-Earn system?

AA manufactures computers. These are sold to BB at $100 a computer plus a 5% sales tax. BB subsequently sells the computers to CC for $200 a computer plus a 5% sales tax. C sells the computers to customers at $300 a computer plus a 5% sales tax.

The total tax received by the tax authority is $30.

Which type of tax is described above?

Which TWO of the following are implications of employee income tax being paid to the tax authority through a Pay-As-You-Earn scheme?

An entity purchased equipment on 1 April 20X4 for $200,000. The equipment was depreciated using the reducing balance method at 20% a year.

Depreciation was charged up to and including 31 March 20X7. At that date the recoverable amount of the equipment was $94,000.

Calculate the impairment loss on the equipment in accordance with IAS 36 Impairment of Assets.

Give your answer to the nearest whole $.

Which of the following statements about trade payables management is false?